What gets me excited in a startup pitch

I have now seen nearly 1,000 startup pitches, and unfortunately only a few of them are memorable. To get me fully present, the entrepreneur needs to catch me in the first 5-minutes.

I need to sense the excitement, presence and cohesiveness between what that entrepreneur is building and her personal narrative. That’s what gets me curious to learn more, to ask provoking questions and to mentor that founder and team in their next steps.

Nonetheless, as a professional investor, I need to work with a clear framework to analyze early stage startups to maintain consistency and avoid, as much as possible, biases that impact my judgement (i.e. affinity with the founder story). This framework, or scorecard, is structured to allow me to collect the relevant data points and criteria to later discuss the startup with my investment team and to help me build enough conviction to make decisions faster, either to advance it or to drop the deal.

Note: In this post I am focusing on early stage startups because when I analyze later stage companies (series B+) the data should tell the story better than the entrepreneurs, and the relevance of the initial narrative is diminished in comparison.

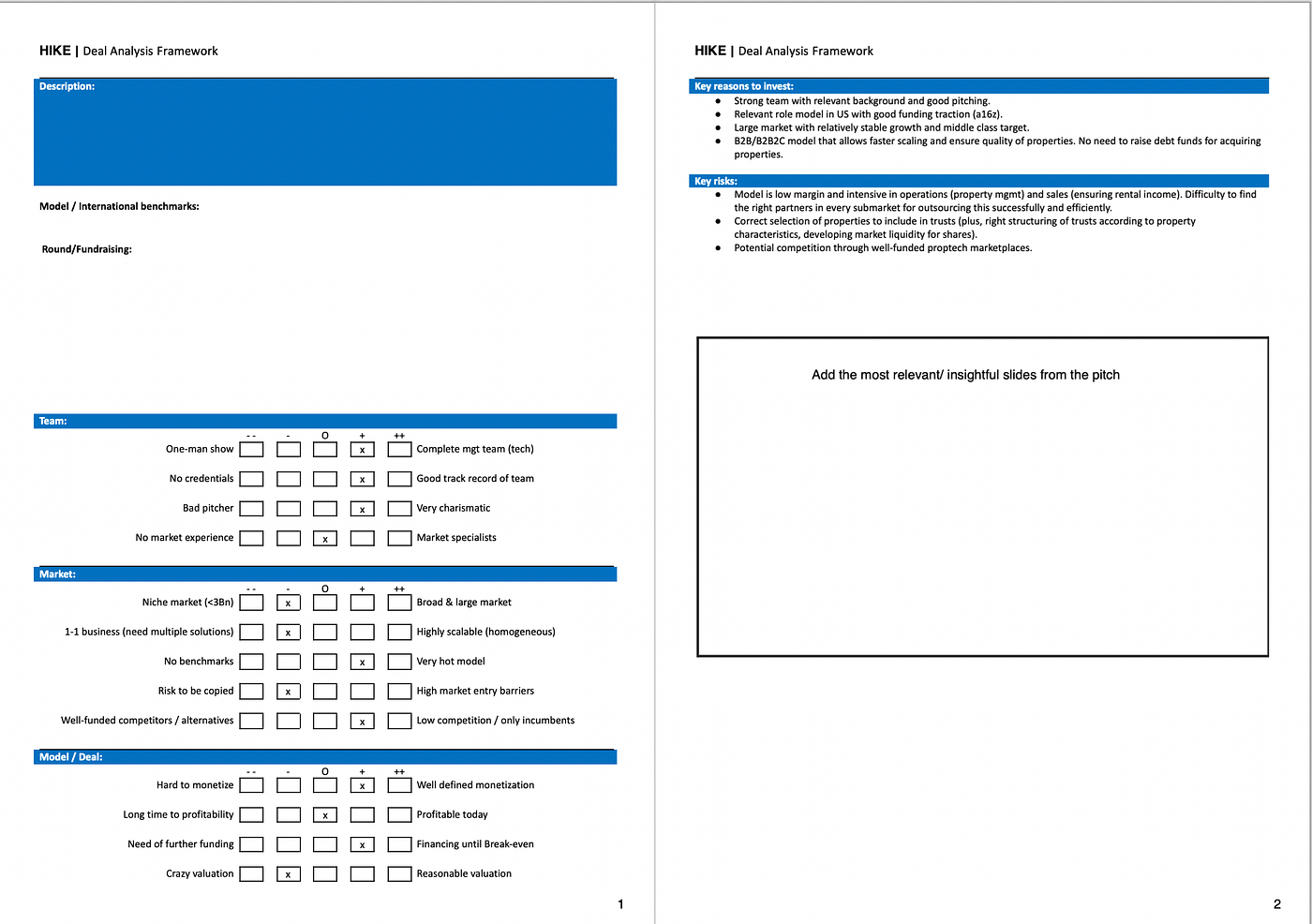

So here we go with the framework. After listening to the entrepreneurs introduction, which I expect to be brief but full of life, I need to be able to quickly put on paper what the company does: the problem it is solving, who it is solving for and how is that specific market. This comes in text format in the Description, as seen below.

Also relevant to my analysis of the model is to understand whether that startup is inspired by an international successful company. This is important for what I will do after the first interaction, which is to enrich my analysis by double-checking all the critical data-points that were sold to me during the pitch (i.e. market size, why benchmark model was successful elsewhere, etc). This comes into Model/ International benchmarks.

Round/ Fundraising allows me to detail what’s the company funding history and what the entrepreneur is looking for in this round. I have always tried to be honest and upfront with founders if I find that their funding expectations are unrealistic, but in reality most founders are stubborn by nature and need to go to market and test waters before adjusting round size and price. I also always highlight that the price is set by the market, and is determined by how much investors are willing to pay. On the other hand, it’s important to be careful and to not burn bridges. Investors will find strange if you show up today asking for a $3M seed round at $15M pre-money in your pre-operational startup, and next month decide to raise “only” $1M at $8M post-money as you want to “close the fundraising process to get back to operations”. Listening to an independent advisor can be helpful as most investors won’t be as honest and direct as I typically am.

Then we move to mostly qualitative criteria that reflect the strength of the (1) Team, (2) Market, (3) Model and (4) Deal attractiveness.

1. Team: As most investors will agree with me, the Team is always the most critical element. We are investing for the long-run, a lot will happen until then and we expect teams to reinvent themselves, their teams and their businesses multiple times. As noticed below, a complete management team with a solid CTO is much preferred than a one-man show. Credentials will serve as a reference of an entrepreneur’s ambition, work ethic and IQ. The ability to pitch well and charm the investor is also extremely important as the entrepreneur will likely have to raise multiple rounds in the future. Having the skill to sell the entrepreneur’s story and dreams in an objective yet passionate fashion will highly impact the speed and terms of future rounds (is that founder good at creating FOMO among investors?).

2. Market: You may have heard “An amazing team in a shitty market? Market wins“. This is true, unless founders pivot to a completely different model with plenty of cash available, but this is not what investors are betting at when they make an investment decision. The market size — to be clear, not the larger addressable market, but the specific market for the specific problem you’re trying to solve — matters a lot as investors need to predict how big can that company be in the next 5–10 years. Specifically, I will look into market size, homogeneity of the solution (highly scalable or needs customization to each customer?), maturity of the model, defensibility (what is defensible about the model for this particular team? what assets are hard to copy?) and competition.

3. Model: Double-clicking on the model, I will look into monetization, unit economics and need of additional capital. In today’s world investors are shying away from models that are capital intensive and that need scale to bloom. A great read that illustrates the importance of working with a model that resonates with the current economic and funding environment is Neta’s post-mortem. What I will have to understand is how this business gets easier to run and more capital efficient at scale.

4. Deal: Lastly, I will judge how attractive are the deal terms of that particular pitch: is the valuation reasonable, given what we are seeing the market, or is it crazy? Investors need to be realistic about how that company could exit the portfolio 7–10 years down the road. In general, I need to believe that I will have at least a 10X return on that early stage investment, and I have a good sense of how much most VC-backed companies are sold for at exit point (and it is not anything close to what we’ve seen with the likes of Nubank).

All these points should allow me to highlight Key Reasons to Invest and Key Risks, which should give me the conviction to (a) drop it, (b) introduce it to more people in the team to enrich my initial analysis or (c) push it forward to investment committee. By the end of the day, I am asking myself “would I invest my own money?“. If I am advancing, the answer should always be a clear YES. Asking myself this question allows me to also feel in my guts how much I like that team, company and deal, complementing my intellectual analysis with my gut instinct. In fact, I have co-invested as an angel with GFC in more than 10 companies. If I believe in my work, I should put my money where my mouth is, right?

Leave a Reply

Want to join the discussion?Feel free to contribute!